Identifying Spreads.: How about showing the number of trades contracts for the dark-pool-data (or allow to show all columns from the feed, for that matter.)

Moin Moin.

In order to be able to see/estimate spreads within the dark-pool-data, it would be helpful to be showing the number of trades contracts for the dark-pool-data (or allow to show all columns from the feed, for that matter.).

Maybe we can allow to copy that data to the clipboard in order to paste it into püower-bi, or I can write a little PowerQueryM-Script aggregation the data, or we can use some LLM, in order to see, which patterns are typical for these pairings (As a transformer does not necessarily have to be applied to spoken words, if the floating-point-precision is high enough).

Right now, we do the the premium but not the number of contracts.

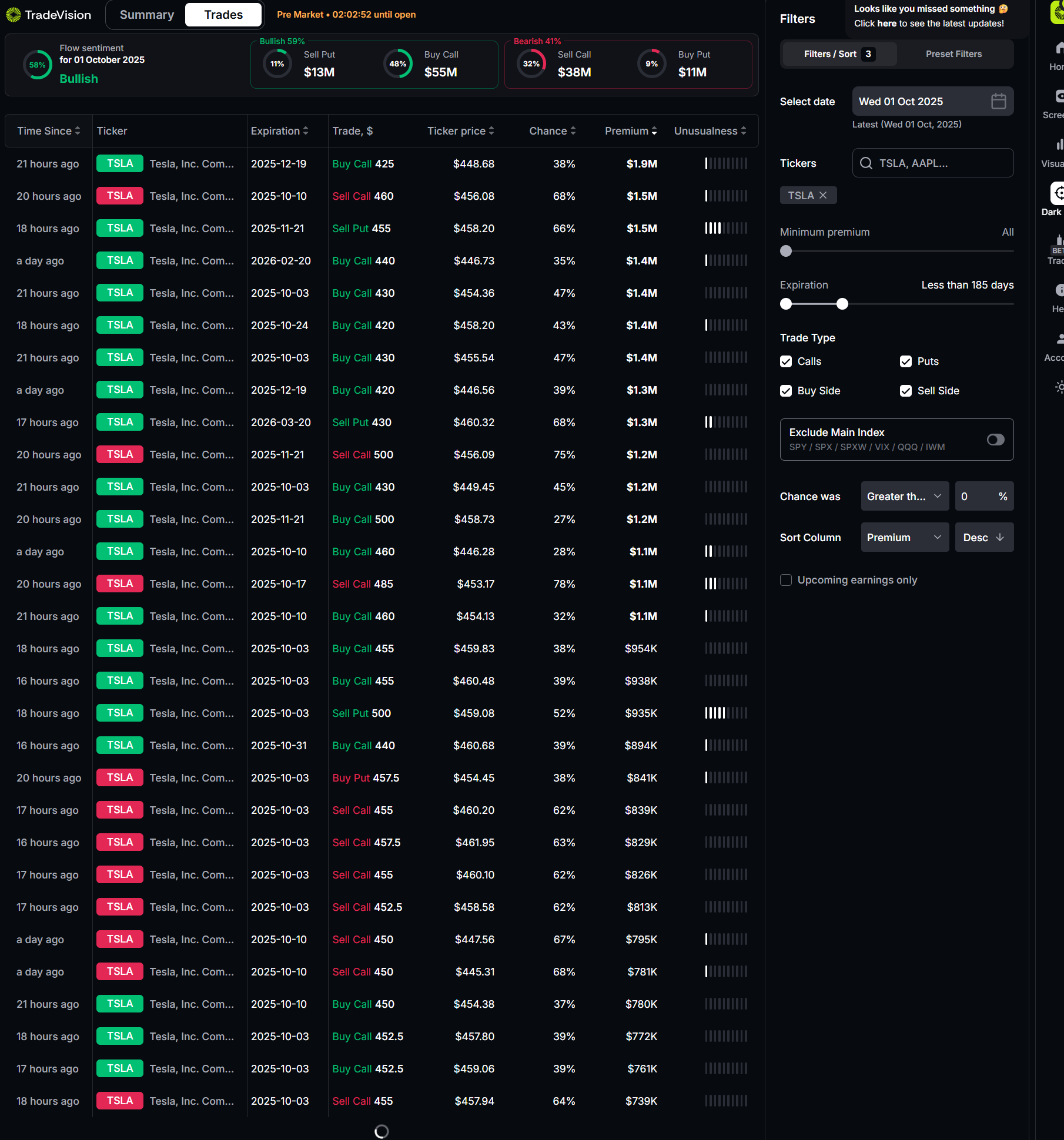

The Screenshot below does show something, that looks like a calendar-spread-pair

1. -TSLAOct10’25@460C

2. +TSLAFeb20’26@440C

So, this is, what I am using, in order to finance a LEAP, which is bullish, despite of the fact, that the TSLAOct10’25@460C is very dangeous with the possibility of the new reduced Model Y coming out, I do think, that this one will have to be rolled out and up.

Cheers,

__Michael.

Please authenticate to join the conversation.

Idea

Feature Request

10 months ago

Michael

Subscribe to post

Get notified by email when there are changes.

Idea

Feature Request

10 months ago

Michael

Subscribe to post

Get notified by email when there are changes.